FINANCIAL INDEPENDENCE IS EASY

- Derek Hagen

- Mar 12

- 4 min read

❝If you live for having it all, what you will have is never enough.❞ -Vicki Robin

Financial independence is less about how much money you have and more about the life that money is meant to support.

FINANCIAL INDEPENDENCE IS EASIER THAN IT LOOKS

Many people talk about financial independence as though it’s some distant, difficult goal.

In the past, we simply called this retirement. It was something that happened later in life... your early or mid-60s, maybe your late 50s if you were lucky.

But financial independence is actually incredibly easy.

Here’s how you do it:

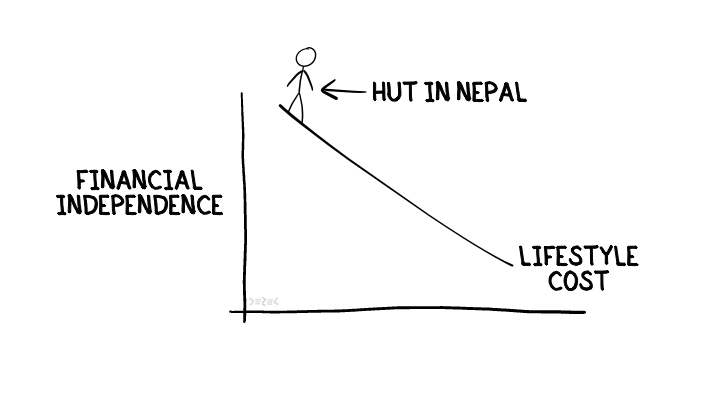

Sell your house, your car, and everything else you own.

Buy a cheap plane ticket to Nepal.

Find a rural village.

Never worry about money again.

You might have to walk a mile to get water. And you probably wouldn’t have many of the comforts you’re used to.

But your money would last the rest of your life. In fact, you might even be the richest person in your village.

If this sounds like a strange thought experiment because you would never actually do it, then it raises an interesting question.

If financial independence is so important, and this is the easiest way to achieve it, why not do it?

The answer is simple.

Most people don’t actually want financial independence. What they want is to maintain a certain lifestyle without having to worry about money.

WHAT FINANCIAL INDEPENDENCE REALLY MEANS

As the Nepal thought experiment highlights, financial independence isn’t quite what we often imagine.

It’s true that having more money makes it more likely that you’ll become financially independent.

But there’s another way to reach financial independence: spend less.

Many people could move to Nepal, live in a small hut, and technically become financially independent.

Because there are two sides to the equation, financial independence isn’t simply about not running out of money.

It’s about maintaining a particular lifestyle.

That means two things matter:

How much money you have

How much your lifestyle costs

THE FINANCIAL INDEPENDENCE EQUATION

Financial independence really comes down to two variables: money and lifestyle cost.

You could think of it like this: Financial independence = money ÷ lifestyle cost.

The more money you have or the less your lifestyle costs, the more likely it is that work becomes optional.

If you have enough money relative to your lifestyle, you move into the work-optional zone.

If your money isn’t high enough or your lifestyle costs too much, you remain in the keep-working zone.

Most of us start somewhere below the line.

Traditional advice says the solution is simple: keep your lifestyle the same and earn and save more money.

Eventually, you reach what people call "your number," the point where you have enough to maintain your lifestyle without working.

But there’s another lever many people overlook.

Instead of only increasing money, you could also reduce lifestyle cost.

That’s what the Nepal thought experiment illustrates.

Of course, these options aren’t mutually exclusive.

You can save more money and choose a more modest lifestyle.

And if your lifestyle increases, the math simply changes. You’ll need even more money to make work optional.

|

|

Money Scripts® are subconscious beliefs we have about money that we learn these we are growing up in our family systems. A Money Script can be anything, but they tend to fall into four categories. Learn what categories your Money Scripts fall into. |

|

|

THE LIFESTYLE QUESTION BEHIND FINANCIAL INDEPENDENCE

The goal isn’t to say that everyone should save more money.

And it isn’t to say that everyone should reduce their lifestyle.

The real goal is awareness.

It’s asking questions like:

Is this the lifestyle I actually want?

Are expectations shaping how I live?

Am I doing things because I value them or because I feel like I’m supposed to?

Once we decide what kind of lifestyle we want, the financial math becomes clearer. We can design the money around the life we want to live.

FINANCIAL INDEPENDENCE IS A LIFESTYLE DECISION

When people think about financial independence—making work optional or retiring—they often treat it as purely a financial decision.

But financial independence is just as much a lifestyle decision.

The first step isn’t figuring out how much money you need. The first step is deciding how you want to live.

Once you’re clear about the life you want, the financial plan becomes much easier to build.

Money doesn’t determine the life. Ideally, the life determines the money.

Financial independence isn't just about reaching a number. It's about deciding what kind of life that number is meant to support.

You get one life; live intentionally.

Interested in more like this? Subscribe and get updates sent directly to you.

If you know someone else who would benefit from reading this, please share it with them. Spread the word, if you think there's a word to spread.

To share via text, social media, or email, simply copy and paste the following link:

REFERENCES AND INFLUENCES

Anthony, Mitch & Paul Armson: Life-Centered Financial Planning

Ariely, Dan & Jeff Kreisler: Dollars and Sense

Crosby, Daniel: The Soul of Wealth

Dunn, Elizabeth & Michael Norton: Happy Money

Hagen, Derek: Your Money, Your Values, and Your Life

Kinder, George & Mary Rowland: Life Planning for You

Klontz, Brad, Rick Kahler & Ted Klontz: Facilitating Financial Health

Perkins, Bill: Die With Zero

Robin, Vicki: Your Money or Your Life

Sinek, Simon: Start With Why

Sinek, Simon, David Mead & Peter Docker: Find Your Why

Wagner, Richard: Financial Planning 3.0